This Recycled Talking Point Is Getting Old

More USD Than BTC Is Used for Criminal Activity, and AML/KYC Can Be Dangerous

A few weeks back, Senator Elizabeth Warren spoke with her buddy Jamie Dimon, CEO of JP Morgan at the recent US Senate Committee on Banking, Housing and Urban Affairs hearing.

In her exchange with Dimon, Warren stated that “crypto is an attractive tool for terrorists, drug traffickers and rogue nations.” Dimon added that “the only true use case for it is criminals, drug traffickers, [anti-]money laundering, tax avoidance.”

(Let us remember that JP Morgan has paid $39 billion in fines, has issued a crypto token and used to move Epstein’s money — all since 2005, under Dimon’s leadership.)

This week, Chair of the SEC, Gary Gensler, told CNBC that “amongst [Bitcoin’s] use cases is really for illicit activity — money laundering and sanctions [evasions] and ransomeware and the like.”

And Senator Warren recently added to the “Bitcoin is for money launderers” narrative on X.

(Love that community note.)

Here at new renaissance capital, we know that Dimon, Gensler and Warren extremely manipulative people who like to distort facts.

So, let’s take a look at some statistics that debunk the claims of Warren, Dimon and Gensler, the axis of fiat.

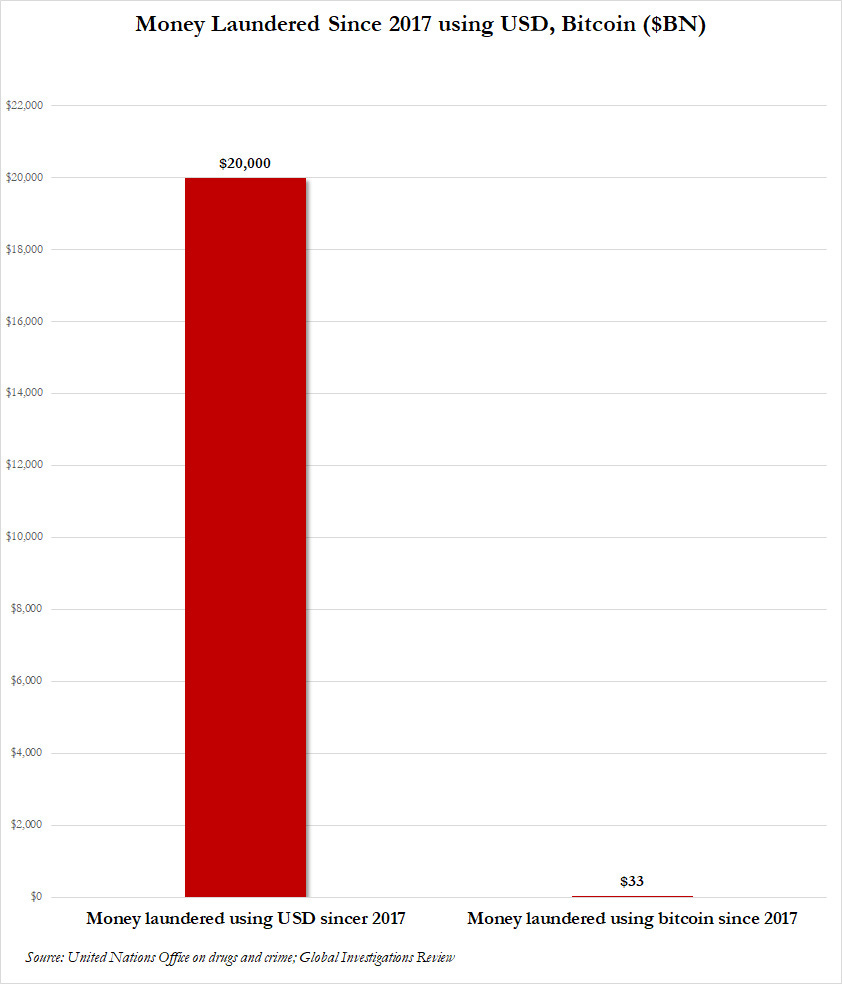

The United Nations found that 60,000% more money is laundered through US dollars than through bitcoin.

Also, as of November 2023, 70% of bitcoin’s supply hadn’t moved for over a year, which means that the primary use case for bitcoin is saving, not criminal activity.

What the likes of Warren, Gensler and Dimon also don’t acknowledge, though, is that activists around the world who’ve been debanked by authoritarian regimes rely on Bitcoin.

And the sort of KYC/AML laws that Warren is pushing for more of can hurt those who need to remain anonymous so to stay out of the crosshairs of their government.

KYC/AML Can Be Dangerous

I discussed the issues around KYC/AML with Lyudmyla Kozlovska and Kasia Szczypska, President and Chief Advocacy Officer of Open Dialogue Foundation, respectively, this week.

(Please subscribe, rate and review the podcast on your preferred platform!)

The Open Dialogue Foundation is an organization based in Belgium that defends human rights, the rule of law and democracy — especially in former Soviet states.

The organization does everything from providing aid to Ukraine to shaping national and international policy to working to free political prisoners.

The members of the organization also support Bitcoin, as they understand that it’s a tremendous tool for those whose government has kicked them out of the traditional financial system.

In our conversation, we discussed the dangers of KYC/AML and why people should not have provide personal information for crypto exchanges the same way they do for banks.

(Personally, I’d like to see less KYC/AML online worldwide in general, as this week, I had to create a free CreditWise account for work and was able to see how many organizations have leaked my personal data onto the dark web. Absolutely petrifying.)

Lyudmyla and Kasia have been speaking with legislators across Europe as well as members of the Financial Action Task Force (FATF) — an intergovernmental organization that works to combat money laundering — in efforts to reduce KYC/AML requirements around Bitcoin/crypto (stablecoins).

I highly recommend that you listen to this interview. I believe it will reshape the way you look at KYC/AML as well as who’s actually using Bitcoin and for what purposes.

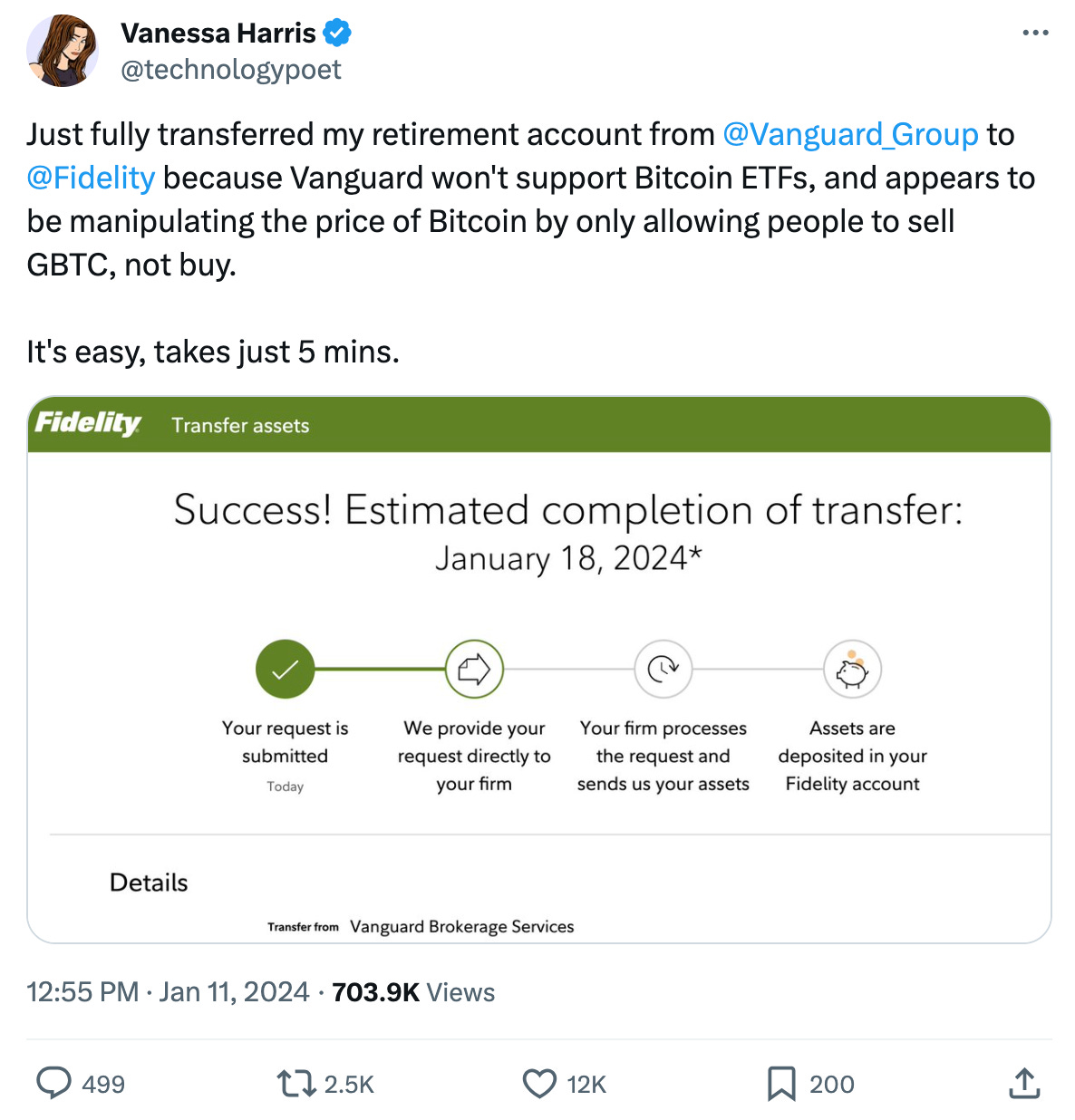

Funds Flee from Vanguard

Once the spot bitcoin ETFs went live this week, Vanguard customers were rudely awakened by the fact that their brokerage wouldn’t let them purchase any of these ETFs.

In response, some moved their funds from Vanguard to more Bitcoin-friendly brokerages like Fidelity.

And they didn’t hesitate to let everyone on X know it.

I shared my thoughts on this topic with MarketWatch on Thursday (link below quote).

As investor interest in bitcoin ETFs appear to be high, financial institutions that don’t offer access to the trading of such products may suffer from user outflows, said Frank Corva, senior analyst for digital assets at comparison website Finder.com.

“Financial institutions that ignore bitcoin and hinder their clients from getting access to the asset will likely be punished in the form of their clients moving their money to institutions that accommodate their desire to get exposure to bitcoin,” Corva wrote in emailed comments.

Full article: “Vanguard’s decision to shun triggers backlash — with some customers moving to crypto-friendly competitors like Fidelity” (MarketWatch)

We’re no longer in an age in which TradFi can ignore Bitcoin.

The platforms that do will do so to their own detriment.

Thanks for reading the free portion of this edition of the newsletter.

Please feel free to send a few Sats if you found it helpful: newrencap@blink.sv

Let’s go to markets:

Keep reading with a 7-day free trial

Subscribe to Frank Corva's Newsletter to keep reading this post and get 7 days of free access to the full post archives.