Meet the Guilty Parties: Wall Street Traders and Government Regulators

Nothing Has Changed

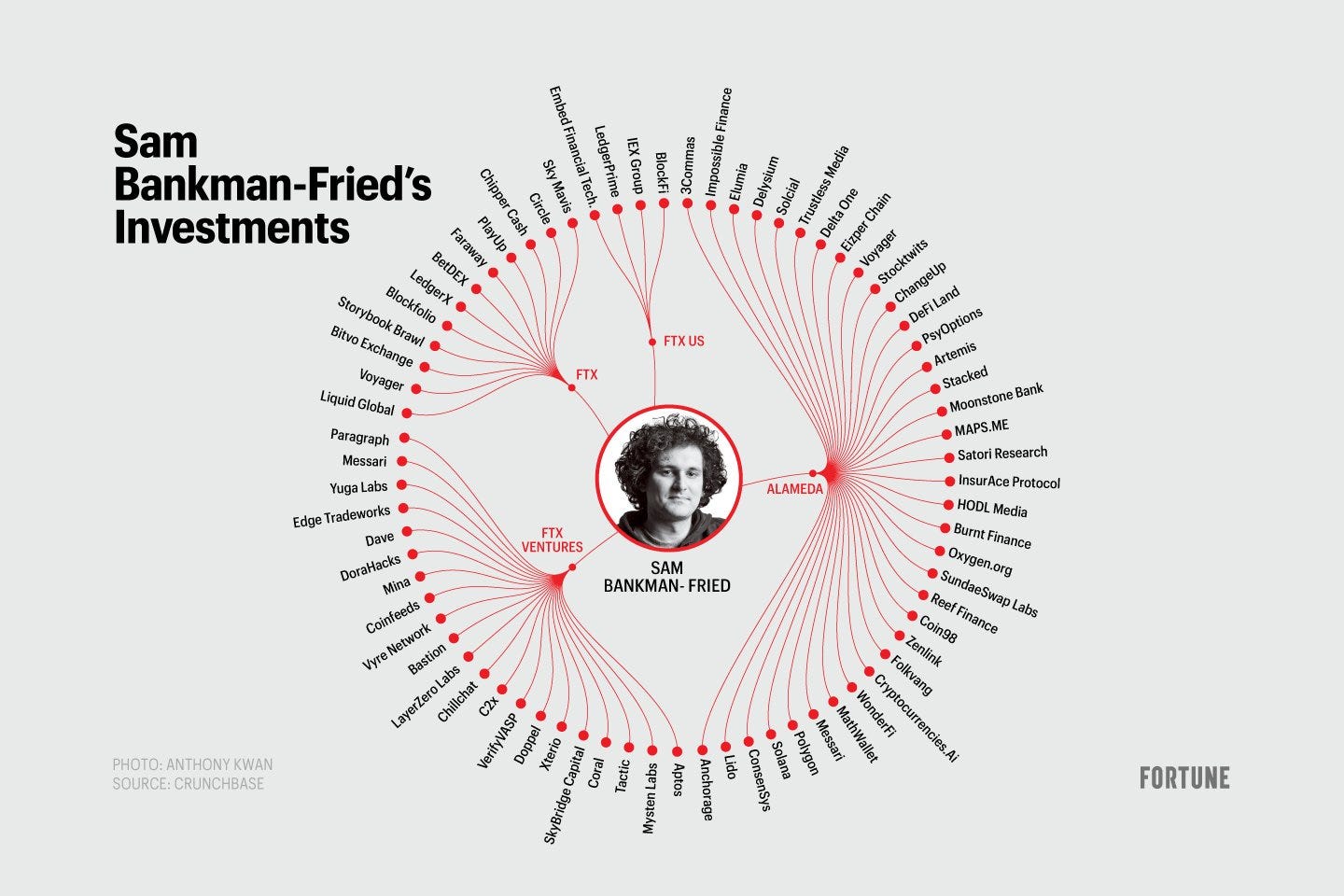

FTX — formerly one of the three biggest crypto exchanges in the world — has filed for Chapter 11 bankruptcy.

Alameda Research — formerly one of the biggest crypto hedge funds in the world — has also filed for Chapter 11 bankruptcy.

What the two entities in common is that they were both started by Sam Bankman-Fried (SBF).

Now that these two entities have failed, SBF and co. will likely take down with them not just the many retail investors whom they scammed, but the many entities that they invested in — as well as the entities that invested in them.

If you’d like an account of what catalyzed the collapse of FTX, I wrote one in the now inaptly titled article “Binance to purchase FTX is bailout offer.”

If you’d like a more up to date take on the matter, Google “FTX collapse” and you’ll find yourself presented with a host of articles that outline what’s transpired.

You can also watch the following video to get the gist of it:

The tweet below pretty much sums it up, as well:

I’m not going to go too deep into the details of what’s happened in this edition of the newsletter.

Instead, I’m going to discuss who’s to blame in this tragedy.

The guilty parties include those who entered crypto with a Wall Street trader mindset and government regulators who’ve done very little to protect crypto investors.

I’ll also discuss what you can do to mitigate the multidimensional risk inherent in investing in crypto and how you can avoid becoming a victim of the SBFs of the world.

Let’s start with the Wall Street trader types.

Wall Street traders

Zhu Su and Kyle Davies — the former heads of the now bankrupt crypto hedge fund Three Arrows Capital, who leveraged borrowed digital assets for trades — were former traders at Credit Suisse.

Alex Mashinsky — the former CEO of the now defunct crypto lending platform Celsius, who leveraged his clients’ digital assets for trading — didn’t ever technically work on Wall Street, but he was known for taking leveraged bets on emerging technologies.

For more on Zhu, Davies and Mashinsky, please read the previous edition of this newsletter: “This Cycle’s Cleansing”

And now we have Sam Bankman-Fried (SBF) — the former CEO of FTX, who is reported to have committed massive fraud — an MIT grad who worked on Wall Street as a quant trader before getting into crypto.

Fun fact: SBF didn’t even know what blockchain was before he started trading digital assets.

I assume that Bankman-Fried did fairly well trading crypto with leverage when he ran Alameda, the same way he probably used leverage while trading traditional assets when he was a quant trader on Wall Street.

And FTX offered leveraged trading to its customers.

Leveraged trading in crypto markets is dangerous on various levels, though — both when retail users use it and when crypto firms use client funds as collateral for it.

I discussed this in “Once More for the People in the Back: Get Your Digital Assets off Centralized Exchanges,” an article I wrote for Nasdaq on behalf of Finder this week.

Below is an excerpt from the piece:

"Leverage and BTC don’t mix…

BTC is a volatile asset. Because of this, it doesn’t work well as collateral in leveraged trades…

And when you leave the private keys for your BTC in the hands of an offshore entity like FTX — one that operates outside of the purview of U.S. regulation — you are vulnerable to the exchange using the BTC that it custodies for you as leverage in its own transactions or trades, as unethical as that may be.”

Note: BTC=bitcoin; feel free to substitute any digital asset in place of BTC in the pull quote above

But the real kicker with FTX-Alameda (I connect the two with a hyphen because they seem to have been operating without much division)…

…is that they didn’t actually hold any BTC on their balance sheet.

Okay, maybe they held one bitcoin.

Maybe FTX lent the BTC on its balance sheet to Alameda to use as leverage in trades at one point, and maybe Alameda lost all of the BTC in losing trades. I don’t know what happened yet.

Some of the only good news here is that, because FTX and Alameda don’t have any BTC to liquidate — or sell back to the open market — their implosion may not directly affect the price of BTC.

They did own some other highly illiquid digital assets that they are currently selling, though. One of those assets is Serum (SRM).

The obvious bad news is that FTX customers who purchased BTC through FTX but never took the private keys for their BTC from the custody of FTX will likely never be made whole.

The über-kicker in all of this is that SBF has testified before Congress last year, stating that crypto was different from traditional finance in that there’s complete transparency in the systems that underpin this new asset class.

Here’s some of what SBF had to say:

“One of the really innovative properties of cryptocurrency markets are 24/7 risk-monitoring engines…

We store collateral from our users in a way which is not always done in the traditional financial ecosystem to backstop positions.

And the last thing that I’ll say is that if you look at some of what precipitated some of the 2008 financial crisis, you saw a number of bilateral, bespoke, non-reported transactions happening between financial counterparties, which then got repackaged and re-leveraged again and again and again such that no one knew how much risk was in that system…”

The truth is that there is great transparency in the crypto space, but there isn’t when crypto exchanges don’t issue proof of their reserves (I’ll get to that in a bit).

Regardless, you can see here that SBF was lying about what was happening behind the scenes at FTX and Alameda.

And many in D.C. listened to his every word, as he was the second largest donor to the Democrats in the 2020 election.

Oh, and his parents are apparently two of Sen. Elizabeth Warren’s biggest donors (though, I don’t yet have a source for this yet).

Oh, and the father of Caroline Ellison — the CEO of Alameda as of last week — just happens to have been SEC Chair Gary Gensler’s old boss.

Apparently, Glenn Ellison didn’t pass on his smart genes, though…

Anyway, let’s move on to the second group I wanted to discuss: government regulators

Government regulators

Gary Gensler has been an outspoken critic of crypto. This is hardly a secret.

Instead of proposing a proper framework to govern the crypto industry, he’s “regulated by enforcement,” which means that he’s arbitrarily penalized crypto companies whenever he’s felt inclined.

Some have argued Gensler has acted in an unconstitutional way.

This has left the crypto industry nervous about what he’ll do next, which is 1.) wildly unfair and 2.) probably the way he wanted it.

Sen. Warren has been behind Gensler every step of the way.

Because US regulators haven’t issued proper guidance, many entities have gone offshore. FTX was one of these entities.

When entities go offshore, they aren’t subject to US regulatory scrutiny, which means they can get away with being less transparent with their bookkeeping.

The opposite of something like FTX — an opaque centralized finance (CeFi) entity — is decentralized finance (DeFi), where all transactions are made via smart contracts and recorded publicly on the blockchain.

Ironically, Sam Bankman-Fried had been working on legislation that would have made it more difficult for users to engage with DeFi protocols.

Because of that, some — like Congressman Tom Emmer — believe that Gensler may have been working behind closed doors with SBF.

US Senate candidate Bruce Fenton may have put some of the pieces together in the tweet below…

…though, I’m not wholly convinced of this conspiracy theory.

But if it comes out that Gensler was working behind closed doors with SBF, you can likely expect chaos (at least on Twitter — which doesn’t really mean much if we’re talking real talk.)

SBF also “lobbied” regulators in his efforts to craft a regulatory regime that would have been favorable to FTX — and not so much for other players in the space.

The sad truth in all of this is that when you commit fraud as the head of a financial institution in the US — and throughout most of the world — you don’t really get punished for it.

So, we probably shouldn’t get our hopes up that SBF will be brought to justice for what he’s done.

Given how close he and his girl Caroline are to the likes of Gensler and Warren, you can bet they’ll likely be protected from any sort of harsh punishment.

At the same time, many people will call for more regulation of crypto now. But let me ask you this…

What did regulators do to protect us from Great Financial Crisis of 2008? (Hint: Nothing.)

What did regulators do to punish those who caused the Great Financial Crisis of 2008? (Hint: Very little, if anything.)

What we need to crypto isn’t further regulation. Instead, we need transparency. (Yes, sure, regulators can mandate this transparency.)

Exchanges should be pressured to make the wallet addresses that hold their reserves public so that everyone can see what they are holding on their balance sheet.

Exchanges should be clear about which and how much fiat currency they hold on their balance sheets, as well, as sometimes users leave cash balances on exchanges.

If exchanges don’t do these things, people shouldn’t use said exchanges.

And once people do find an exchange that’s best for them and buy assets on said exchange, they should then quickly move the private keys for the assets that they purchase into a noncustodial wallet.

This brings me to the last point I want to make.

(Before I continue, though, please also note that if Gensler really wanted to keep retail investors safe at least in regard to their investing in bitcoin, he could have approved a spot Bitcoin ETF in which investors could have invested in an ETF backed by a trusted custodian for the asset. But he didn’t. I wrote about this more here for Nasdaq on behalf of Finder: “SEC Rejects Application to Convert Greyscale Bitcoin Trust (GBTC) into a Spot ETF”

Understanding your responsibility

As I wrote in the aforementioned “Once More for the People in the Back…” piece, there are a number of benefits to storing the private keys to your digital assets in a noncustodial wallet.

I’m not going to outline them here for you (read the piece to learn what they are), but the primary one is that you you must hold the private keys to your digital assets to actually have ownership over them.

I’ll likely be making a video soon for how to move the private keys from an exchange to a noncustodial wallet.

In the meantime, if you’re invested in crypto and don’t own a noncustodial hardware wallet, the Ledger Nano S Plus provides the best value for your money IMHO.

Google “How to use a Ledger Nano S Plus” to learn more about how to use the device.

Nothing has changed

What we just saw happen with SBF and co. has little to nothing to do with crypto.

In fact, nothing has changed in the nature of crypto networks and systems.

Bitcoin is still operating as it was intended to, producing a block of transactions approximately every 10 minutes, while computing power from around the globe maintains its permissionless and immutable network.

And DeFi is still functioning smoothly.

The notable issue at hand is that nothing has changed amongst the Wall Street trader types in the crypto space, nor with government regulators.

The Wall Street types are still doing fraudulent Wall Street-type things.

Regulators still aren’t regulating properly, nor are they punishing people who act fraudulently.

Yes, the prices of digital assets have fluctuated greatly as a result of this catastrophe, and we likely haven’t seen the worst of it, so please be careful out there.

But if we were to look at this event from a different angle, we could say that the space is now healthier due to more leverage and fraudulent actors being flushed out of it.

What just happened with FTX-Alameda is what should more often happen with traditional financial institutions but doesn’t.

It doesn’t mostly because of the revolving door between members of those institutions and US regulatory agencies and because these institutions know that the Fed will bail them out if and when worse comes to worst.

Traditional finance is rife with moral hazard because actors in the space believe that an eternal backstop from the Fed exists.

Bitcoin was created in response to the fraud in our financial, regulatory and political systems. This hasn’t changed.

And my views on the value of BTC in the long-term haven’t changed.

I’m positive that I’m not the only one who feels this way.

The events of this past week may set the digital asset industry back quite a bit, but, as I said, what transpired is a good thing if it flushes the leverage and bad players out of the system.

That being said, I know this hurts, and I hope everyone is okay out there.

Best,

Frank

Twitter: @frankcorva

Currently watching: